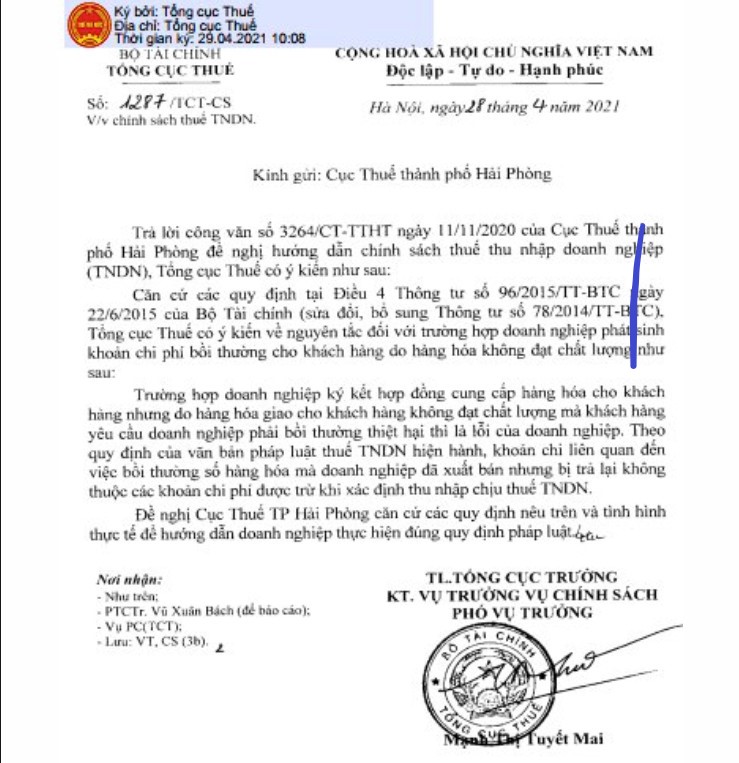

Official letter 1287/TCT-CS about the compensation for the goods that do not meet the quality as follows:

In case, an enterprise signs a contract to supply goods to a customer but the goods delivered to the customer are not of good quality and the customer requires the enterprise to compensate for damage, it is the fault of the enterprise. According to the current legal documents on corporate income tax, the expenses related to the compensation for goods that the enterprise has sold but returned are not included in the deductible expenses when determining taxable income..

VN

VN EN

EN 中文

中文 한국어

한국어 日本語

日本語

{kind=link}